Smells Like Teen Spirit

w.306 | Vanguard & Chill, Capital Intensity, Seed Valuations, & Vintages

Dear Friends,

‘Boy has our vanguard and chill strat been working,’ my friend texted me this week, which is how I’ve felt for a while investing-wise. Now that Iran-war uncertainty is trending down, it's back to business as usual, although valuations are just as historically high as before. The FT calls this ‘an Earnings Before Iran, Tariffs and Dubious Announcements (ebitda) Mentality,’ which I like.

Since we are all long-term, diversified, buy-and-hold investors, the only fun game left is finding uncorrelated, high-upside additions or something more personal and impactful to invest in.

A good reminder of what we are doing.

Today's Contents:

Sensible Investing

Weeklies: Selfie & Song

Sensible Investing

I recently attended a conference on late-stage private software and internet companies in San Francisco, hosted by the research department of a prominent investment bank. These gatherings are great for taking the temperature of pre-IPO companies. The audience is more discerning and analytical than your average VC. Here are my takeaways on four types of companies.

First, is this a science experiment going anywhere? Fusion, Quantum, Photonic-things. I get it, these guys are smart, SMART! Genius maybe. Who knows. But, like, what's the actual revenue here, and am I still taking science risk? Is late capital going to get any return for this? In the current market, it seems like yes. But market timing is tricky, and exits are hard. Look no further than this recent TechCrunch article, ‘Cracks are starting to form on fusion energy’s funding boom.’

Second, war is everywhere, and there is a defense spending bonanza. All the defense tech and many ‘American Dynamism’ companies fall in here. So many drones. Lots of dual use. It’s unclear whether the contracts are recurring and whether there are more than one or two true buyers.

Third, (and often overlapping with #1 and #2) Wow, it’s capital intensive. New chip manufacturing, robotics, newly described ‘physical intelligence’, cloud kitchens, etc. I was probing the manager of the venture division of a successful quant crossover fund on the reasoning for a pre-IPO nuclear deal they invested in, and the person said, “I agree with your concerns completely, but our hedge fund energy guys underwrote it because they think they can get a pop in the 6-month IPO window.’ That seems like gambling to me.

Four, AI companies with insane growth numbers, but what are the true unit economics, particularly if model R&D costs depreciate in 3-6 months? And how much of that is the magic “ARR-embellishment”? When asked about the unit economics, a VC said the industry's best guess right now is somewhere between 0% and 60%, which seems like a wide range. A few examples of the potential issues: Cursor (which wasn’t presenting) apparently had -23% gross margins as of Q4 2025, which seems accurate. YC has just issued guidance on ‘being truthful and precise about revenue.’

The last category is all the out-of-favor companies that desire liquidity, i.e., 20-year-old PE-backed companies with no growth, $2-5B valuation companies in crowded categories that aren’t going to grow into the valuation, anything making a profit but with modest (10-30%) growth.

Most people thought the valuations being discussed were completely out of range.

The smartest (and seemingly most honest) speaker was Martin Casano from a16z, who recently gave a nice interview in the FT: "It’s not that hard to build AI models" (PDF). Punchline: Recent progress in AI is an industrial revolution-scale event, but warns that the ability of the bigger players to raise ‘cheap money’ is time-limited.

Okay, so growth looks frothy, but what about the earlier stage:

Is an early-stage venture fund a good bet right now?

Obviously, there is a lot of dispersion, but on average, the answer is no. More than anything, there is absolutely no price discipline, a ton of dilution. I was evaluating a fund recently with a track record that looks like this, bearing in mind moderate scale but still <$75M fund size:

A top-decile 2015 vintage fund 1: 4.5x DPI (~10x TVPI), top three positions at 26x, 75x, 35x.

2019 Fund 2: nothing remarkable, current TVPI 1.2x.

2022 Fund 3 has a bunch of awesome-looking Series B rounds from companies that seem to be doing super well and have raised more than $100 million. TVPI is like 1.07x. A bunch of 4-3x multiples on pre-seed checks after the companies have raised Bs. Yikes.

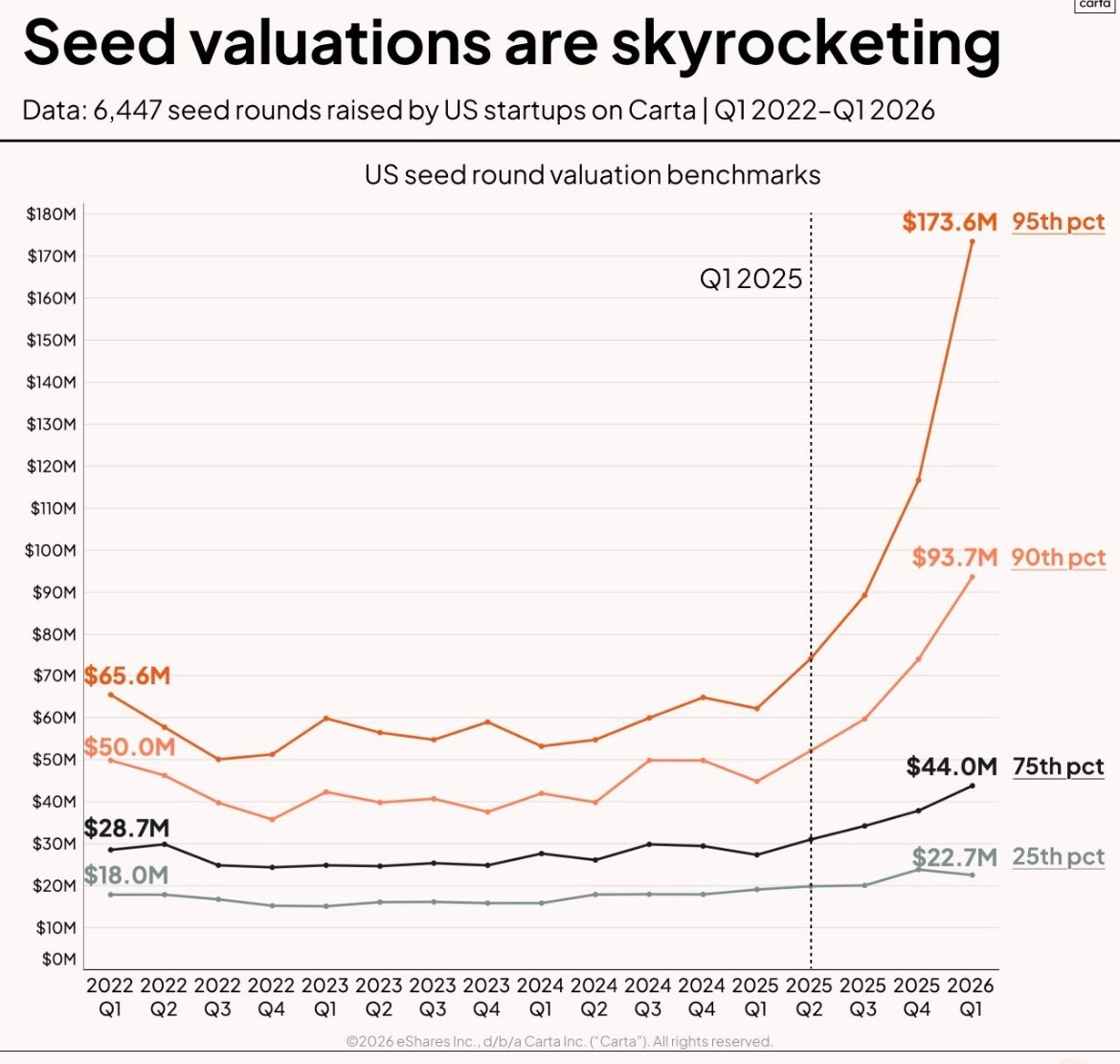

2025 vintage Fund 4, do you invest? No, right? Because the valuations aren’t rewarding the risk. The historical valuation highs are in the Carta data below and are discussed in this recent piece, titled "The Valuation Trap."

BUT, what this fund does do well is SPVs, and this is the game now. Because, as a capital allocator, the risk-reward often in the early stage is just not worth it when winners that emerge only give you 2-4x appreciation between pre-seed and Series B. You should probably be hitting those Series A (and more likely Series Bs) where there is truly breakout potential. And that is what this fund and most funds have been offering.

People liked this piece, The Narrow Path, about the state of seed venture investing and its bifurcation. Same phenomena discussed, longer article.

The person who created the Simpsons meme did it in response to the private credit chart below, for the record. I don’t have any exposure to private credit (other than my own private dealings, where I also have exposure to the equity), so I don’t follow it too closely, but I've always felt this was an obvious market-hype moment, and vindication is satisfying.

Weeklies: Selfie & Song

Selfie: Natchez, Cobain, Elvis, Wearin’ the World

Recently, I was on a mission-critical road trip between Nashville and Austin, making my way through the South with a large stretch on the Natchez Trace Parkway. This 444-mile all-wooded freeway with no stoplights is an under-discussed American gem. It had been a migratory path for bison for 10,000 years. During the Louisiana Purchase era, it became a key wagon thoroughfare for those venturing through the middle of the country. Highly recommend for a history-filled road trip and a scenic drive.

During the trip, I donned my ‘Wearin’ the World’ jacket, which I picked up second-hand on eBay and was made famous in 1989 by Kurt Cobain. I received many compliments on the item from young women working service jobs along the way. It made me think: If I were aged 16-24 today and working as a waitress at the Rattlesnake Saloon in Tuscumbia, AL, how would I go about seeing the world?

A tough question on the face. But these days, there are so many options to change your location - military, nursing, hospitality, childcare, teaching English, tourism. Economic escape is harder, of course, but that is probably figure-outable after leaving. For someone to execute any big change is a lot of will and, assuming you have the basics of literacy and numeracy, skills you can learn as you go. I bet all of them can make a move if they claim the agency. Perhaps their own ‘Wearin’ the World’ jacket could be a constant reminder - or at least a map of where to go next :)

If Elvis rose from poverty in a small town to being an international cultural icon with a lasting legacy, anyone can. That remains true.

Song of the Week:

Here on YouTube (2.1 billion views).

I try to avoid songs that might be seen as trite or overplayed, and this always felt in that category. But in honor of the jacket and the song's meaning, this week seemed fitting. Kurt Cobain vs Elvis Presley is also a demonstration of how dramatically different cultural epochs are. Elvis sang like he meant it. Cobain (and Gen X) made a career out of the suspicion that meaning anything was embarrassing. This Millennial was happy to be around and appreciate both.

There have been numerous possible interpretations, but the leading theory, which Kurt Cobain endorsed, is that it’s a song making fun of the idea of revolution.

The title "Teen Spirit" was inspired by a deodorant brand. Cobain misinterpreted a friend's graffiti, thinking it was a revolutionary slogan. This misunderstanding contributed to the song's ironic tone. There’s a lot of attention-grabbing performance of revolution out there today (and always).

“Smells Like Teen Spirit” by Nirvana

Load up on guns, bring your friends

It's fun to lose and to pretend

She's over-bored, and self-assured

Oh no, I know a dirty wordThanks for reading, friends. Please always be in touch.

As always,

Katelyn

if I had to make a "bet" I would say photonic quantum is probably the closest, even though Willow Lake is promising on Google's end.

how or who makes money is something I definitely cannot predict, there's a ton of hype surrounding the space